Is Credit Karma accurate?

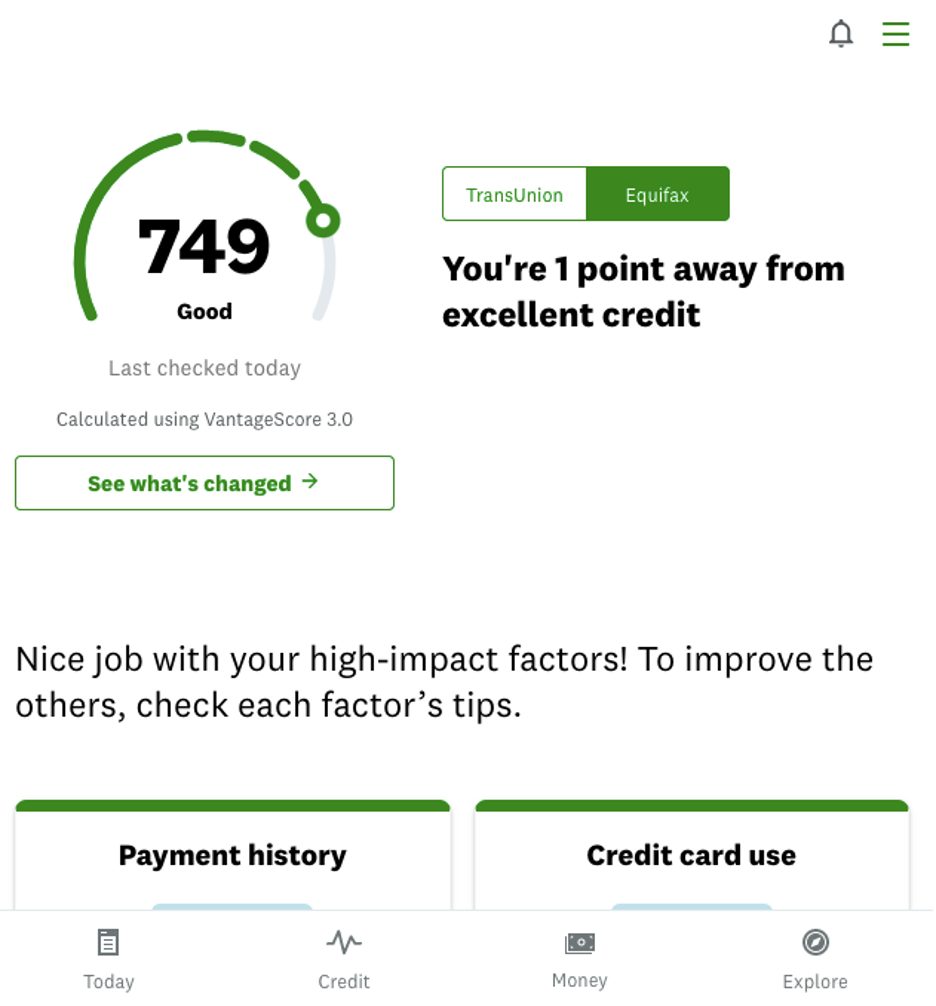

Credit Karma is a free credit monitoring service that provides you with your credit scores and reports from two of the three major credit bureaus, Equifax and TransUnion. It's a great way to keep track of your credit health and see how you're doing over time.

But how accurate is Credit Karma?

The answer is: it depends. Credit Karma's scores are not always 100% accurate, but they're generally pretty close. In a study by the Consumer Financial Protection Bureau, Credit Karma's scores were found to be within 25 points of the FICO scores of 90% of consumers.

There are a few reasons why Credit Karma's scores may not be 100% accurate.

Credit Karma only gets your credit information from two of the three major credit bureaus.

Credit Karma's scores are based on a different credit scoring model than FICO, the most commonly used credit scoring model.

Despite these limitations, Credit Karma's scores are still a valuable tool for tracking your credit health. They can help you see how you're doing over time and identify any areas where you need to improve.

Credit Karma Score Accuracy

Credit Karma is a popular free credit monitoring service that provides users with their credit scores and reports from two of the three major credit bureaus, Equifax and TransUnion. While Credit Karma's scores are generally accurate, there are a few key aspects to keep in mind:

- Data Source: Credit Karma only gets your credit information from two of the three major credit bureaus. This means that your Credit Karma score may not be 100% accurate if there is inaccurate information on your report from the third credit bureau, Experian.

- Scoring Model: Credit Karma's scores are based on a different credit scoring model than FICO, the most commonly used credit scoring model. This means that your Credit Karma score may not be the same as your FICO score.

- Timeliness: Credit Karma's scores are updated monthly. This means that your Credit Karma score may not reflect the most up-to-date information on your credit report.

- Factors Considered: Credit Karma's scores are based on a number of factors, including your payment history, credit utilization, and length of credit history. If any of these factors change, your Credit Karma score may also change.

- Usefulness: Despite these limitations, Credit Karma's scores are still a valuable tool for tracking your credit health. They can help you see how you're doing over time and identify any areas where you need to improve.

- Limitations: It's important to keep in mind that Credit Karma's scores are not a substitute for a FICO score. If you're applying for a loan or other type of credit, lenders will likely use your FICO score to make a decision.

Overall, Credit Karma's score accuracy is generally good, but it's important to be aware of the limitations. By understanding the factors that affect your Credit Karma score, you can use it as a tool to improve your credit health.

1. Data Source

The accuracy of your Credit Karma score is directly tied to the accuracy of the information on your credit report. If there is inaccurate information on your credit report from Experian, the credit bureau that Credit Karma does not get its data from, then your Credit Karma score may not be accurate.

For example, if you have a late payment listed on your Experian credit report, but not on your Equifax or TransUnion credit reports, then your Credit Karma score may not reflect the late payment. This could lead to you getting a lower credit score than you deserve.

It is important to regularly check your credit reports from all three credit bureaus to make sure that the information is accurate. You can get a free copy of your credit reports from each of the three credit bureaus once per year at annualcreditreport.com.

If you find any inaccurate information on your credit reports, you should dispute the information with the credit bureau. You can do this online, by mail, or by phone.

By keeping your credit reports accurate, you can help to ensure that your Credit Karma score is accurate. This will give you a better understanding of your credit health and help you to make informed financial decisions.

2. Scoring Model

The credit scoring model that Credit Karma uses is called the VantageScore. VantageScore is a newer credit scoring model than FICO, and it takes into account a wider range of factors when calculating your score. This means that your Credit Karma score may be different from your FICO score, even if your credit history is the same.

For example, VantageScore gives more weight to recent credit activity than FICO does. This means that if you have recently made a few late payments, your Credit Karma score may be lower than your FICO score. Conversely, if you have recently made a few on-time payments, your Credit Karma score may be higher than your FICO score.

It is important to keep in mind that different lenders may use different credit scoring models. This means that your Credit Karma score may not be the same as the score that a lender uses to make a decision about your loan application.

If you are applying for a loan, it is important to find out what credit scoring model the lender will be using. You can then use that information to determine which credit score is most important for you to focus on.

Here are some tips for improving your Credit Karma score:

- Make all of your payments on time.

- Keep your credit utilization low.

- Don't open too many new credit accounts in a short period of time.

- Dispute any errors on your credit report.

By following these tips, you can improve your Credit Karma score and increase your chances of getting approved for a loan.

3. Timeliness

The timeliness of Credit Karma's scores is an important factor to consider when evaluating their accuracy. Credit Karma's scores are updated monthly, which means that they may not reflect the most recent changes to your credit report.

- Facet 1: Recent Credit Activity

Recent credit activity can have a significant impact on your credit score. For example, if you have recently made a late payment, your credit score may be lower than it would be if you had not made the late payment. Credit Karma's scores may not reflect recent credit activity until the next monthly update.

- Facet 2: Credit Inquiries

Credit inquiries can also affect your credit score. When you apply for a loan or other type of credit, the lender will typically make a hard inquiry on your credit report. Hard inquiries can lower your credit score by a few points. Credit Karma's scores may not reflect recent credit inquiries until the next monthly update.

- Facet 3: Credit Limit Changes

Changes to your credit limits can also affect your credit score. If you have recently increased your credit limit, your credit score may be higher than it would be if you had not increased your credit limit. Credit Karma's scores may not reflect recent credit limit changes until the next monthly update.

- Facet 4: Account Closures

Closing credit accounts can also affect your credit score. If you have recently closed a credit account, your credit score may be lower than it would be if you had not closed the account. Credit Karma's scores may not reflect recent account closures until the next monthly update.

Overall, it is important to keep in mind that Credit Karma's scores may not be the most up-to-date reflection of your creditworthiness. If you are applying for a loan or other type of credit, it is important to request a copy of your credit report from all three credit bureaus to get the most accurate view of your credit history.

4. Factors Considered

Understanding the factors that affect your Credit Karma score is crucial for assessing its accuracy. These factors play a significant role in determining the numerical value assigned to your creditworthiness.

- Facet 1: Payment History

Payment history holds substantial weight in calculating your Credit Karma score. Consistent and timely payments demonstrate responsible credit management, resulting in a higher score. Conversely, late or missed payments negatively impact your score, as they raise concerns about your ability to fulfill financial obligations.

- Facet 2: Credit Utilization

Credit utilization measures the amount of available credit you're using. Keeping your credit utilization low, ideally below 30%, indicates that you're not overextending yourself financially. High credit utilization, on the other hand, can lower your score as it suggests a potential risk of excessive debt.

- Facet 3: Length of Credit History

The length of your credit history refers to the duration of time you've had open credit accounts. A longer credit history generally translates to a higher score, as it demonstrates your experience in managing credit responsibly over an extended period.

- Facet 4: Credit Mix

Credit mix refers to the variety of credit accounts you have, such as credit cards, installment loans, and mortgages. Having a mix of credit types can positively impact your score, as it indicates your ability to handle different types of credit responsibly.

These factors collectively contribute to your Credit Karma score and provide insights into your overall creditworthiness. Regular monitoring of these factors and taking steps to improve them can help you maintain a high and accurate Credit Karma score.

5. Usefulness

Credit Karma's scores, despite their limitations, provide valuable insights into your credit health. By tracking your Credit Karma score over time, you can observe trends and patterns in your credit behavior. This allows you to identify areas where you excel and areas where improvement is necessary.

For instance, if you notice a consistent upward trend in your Credit Karma score, it indicates that you are managing your credit responsibly. Conversely, a downward trend may signal potential issues that require attention. By recognizing these patterns, you can take proactive steps to improve your credit habits.

Furthermore, Credit Karma's scores can help you identify specific factors that are positively or negatively impacting your score. By understanding the contributing factors, you can develop targeted strategies to enhance your creditworthiness. For example, if your credit utilization is high, you can focus on paying down debt and reducing your overall credit usage.

In conclusion, while Credit Karma's scores may not be 100% accurate, they remain a useful tool for monitoring your credit health. By tracking your score over time and understanding the underlying factors that influence it, you can make informed decisions to improve your creditworthiness and achieve your financial goals.

6. Limitations

Credit Karma's scores are not a substitute for a FICO score. FICO scores are the industry standard for credit scoring and are used by the vast majority of lenders. When you apply for a loan, credit card, or other type of credit, the lender will likely use your FICO score to make a decision about whether to approve your application and what interest rate to offer you.

Credit Karma's scores are based on a different credit scoring model than FICO scores. This means that your Credit Karma score may be different from your FICO score, even if your credit history is the same. In general, Credit Karma's scores are considered to be less accurate than FICO scores.

There are a number of reasons why Credit Karma's scores may be less accurate than FICO scores. One reason is that Credit Karma only gets your credit information from two of the three major credit bureaus. This means that Credit Karma may not have access to all of the information that lenders use to calculate your FICO score.

Another reason why Credit Karma's scores may be less accurate than FICO scores is that Credit Karma uses a different credit scoring model. This means that Credit Karma may weigh different factors more heavily than FICO does. For example, Credit Karma may place more emphasis on recent credit activity than FICO does.

If you are applying for a loan or other type of credit, it is important to keep in mind that lenders will likely use your FICO score to make a decision. This means that you should not rely solely on your Credit Karma score when making financial decisions.

Frequently Asked Questions (FAQs) about Credit Karma Score Accuracy

This section addresses common questions and misconceptions regarding the accuracy of Credit Karma scores. By providing clear and informative answers, we aim to enhance your understanding and empower you with the knowledge necessary to make informed financial decisions.

Question 1: How accurate are Credit Karma scores?

While Credit Karma's scores generally provide a fair representation of your creditworthiness, it's important to note that they may not always align exactly with your FICO score, which is the industry standard used by most lenders.

Question 2: Why might my Credit Karma score differ from my FICO score?

Credit Karma utilizes a different credit scoring model and obtains data from a subset of the credit bureaus compared to FICO. These variations can contribute to discrepancies between the two scores.

Question 3: Can I rely solely on my Credit Karma score when applying for credit?

While Credit Karma scores offer valuable insights, it's crucial to recognize that lenders primarily rely on FICO scores during the credit application process. Therefore, it's advisable to obtain your FICO score directly from the credit bureaus for the most accurate assessment.

Question 4: How can I improve the accuracy of my Credit Karma score?

Maintaining accurate personal information, disputing any errors on your credit report, and practicing responsible credit habits can contribute to a more accurate Credit Karma score.

Question 5: What limitations should I be aware of when using Credit Karma scores?

Credit Karma scores may not reflect the most up-to-date information, and they do not consider all the factors that lenders evaluate. Additionally, Credit Karma only accesses data from two out of the three major credit bureaus.

Understanding these aspects of Credit Karma score accuracy empowers you to make informed decisions about your credit management and financial well-being.

Credit Karma Score Accuracy

In this article, we have delved into the intricacies of Credit Karma score accuracy, examining its nuances and providing valuable insights. While Credit Karma scores offer a convenient and accessible way to monitor your credit health, it is essential to understand their limitations and how they compare to industry-standard FICO scores.

Remember that Credit Karma scores may not always align perfectly with FICO scores, and lenders typically rely on FICO scores when making credit decisions. By maintaining accurate personal information, disputing errors on your credit report, and practicing responsible credit habits, you can contribute to a more accurate Credit Karma score. However, it is crucial to obtain your FICO score directly from the credit bureaus for the most precise assessment of your creditworthiness.

Understanding the complexities of Credit Karma score accuracy empowers you to navigate the world of credit management with confidence. By leveraging this knowledge, you can make informed financial decisions that support your long-term financial well-being.